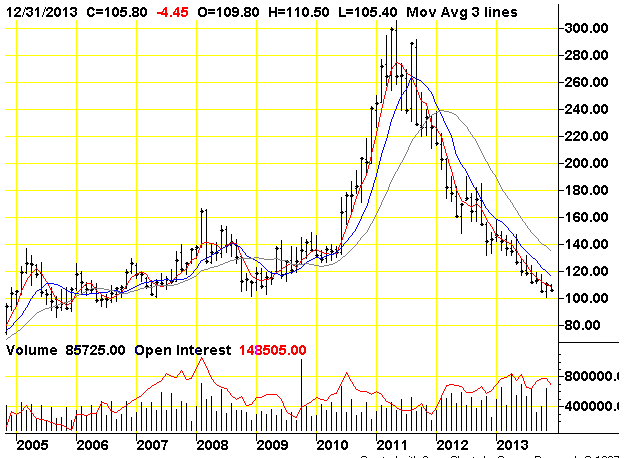

Over the last two years, the C-price (commodity grade price) of coffee has sharply declined. This has had some unforeseen consequences.

The Cycle of Boom and Bust

The fall was precipitated by a bubble-like price spike, which led farmers to bring more land under cultivation and transfer lands used for other crops to coffee production. New lands shifted to coffee production take up to five years before the coffee trees are fully productive. This lag made it difficult for farmers to judge how the market would react to the new production capacity, and as a result, the aforementioned sharp decline in commodity level coffee prices occurred. Yet the coffee we deal with hasn't fallen in price.

Here's Why:

The market for the higher-end coffee Joyride sells has grown during the same two year period, as an international coffee culture has emerged with a focus on varietal, processing and terroir. Simply put, most of the new production that came on line isn't up to snuff. Luckily, we are seeing that beginning to change.

Part of the ethos of Direct Trade is the idea of year-by-year amelioration due to improved farming practices, and improved infrastructure. This process is beneficial for farmers, who can command ever higher prices for their beans. Some of these farmers have also moved away from national contracts (where they agree to only sell to a single roaster in a given country), which has increased prices through competition for the same beans. Unfortunately for us, these two factors mean that many of the coffees we have come to love have reached a price points (say $25+/lb retail) that are too high for most of our customers.

The Sourcers Strike Back

Companies who practice Direct Trade, like our own Stumptown, Intelligentsia and Counter Culture have realized that their menu prices cannot simply skyrocket every year. To balance these appropriately more expensive coffees, many of their sourcers have begun to look for what I call the Second Generation of Direct-Trade Partnerships.

That name can be misleading, since there is no given "Generation" for direct trade and farms are added to the programs every year. But the gist of it is, that as many Direct Trade producers have reached a premium or super-premium level, a second crop of producers has come online. These are great new coffees, often from areas, like Peru, which were not previously known for high quality coffees. For me, these changes are very exciting: I get to see brand new coffees from less famous regions at affordable prices. But where does the falling C-price figure into this?

Rich Farmer, Poor Farmer

Essentially, farmers who sell higher premium beans are not being hit with the price glut in the same way. Although some lots from Direct-Trade farms that don't make the quality cut are often sold on a C-price market, the higher premium paid for the better beans has mitigated the downturn for these producers. As a result, the farmers with better beans have become more prosperous as those around them have struggled.

These farmers have started to acquire land from their neighbors, to benefit from their improved practices and infrastructure, and if anything, the disjoint in pricing has incentivized the practice. We have seen the outcome of this amalgamation go both ways: certain farms have purchased neighboring estates, leading to great coffees that come in bigger (and, for us, more manageable) lots. At the same time, we have also seen coffee quality suffer from farms who were too vigorous in acquiring land, and who were unable to give their new holding the necessary attention and capital needed to produce amazing coffee.

Other collaborations involve farms investing in milling equipment, which allows them to charge their neighbors for the use of the machines. This has a two-fold benefit of increasing community interaction and practical exchange, as well as improving lower-quality coffees, simply by virtue of better processing. In Ethiopia, the ownership structures are somewhat different and many of these mills are owned by a co-operative of the farmers who share them, though the essential effect is identical.

New Beans, Better Beans, Better Prices

The effective result of the price crash has really been positive for specialty coffee drinkers:

1. As older relationships have slowly lofted out of a comfortable price point, new coffees have grown up to fill it.

2. The prosperity caused by Direct Trade producers has grown relative to their neighbors and has led to a greater interest in better production, as well as increasing access to better processing equipment.

3. Finally, these new coffees are coming in at a price where people like me can afford to drink them.

The slump in coffee prices can't last forever. China is becoming an ever-larger coffee consuming nation. The amount of land suitable for growing high-quality coffee (high altitude, appropriate climate) is finite and can't feasibly be increased through human intervention. Finally, climate change has already started to wreck havoc in certain regions, and there is no reason to think these disruptions will soften over time. While we may be looking at higher prices for coffee in the future, for now we can sit back and enjoy great cups from great newly Direct Trade producers.

Written by Joyride Co-Founder Adam Belanich